I recall looking at a spreadsheet at the end of 2023 and being totally overwhelmed. My accounts, investments and bills were a jumbled mess. I was making lots of money, but I did not know where it was going. It was like attempting to find your way into a dense forest without a map. Then, I gave an AI the reins, and he has completely changed my financial life.

What is the Problem AI Finance Tools Are Solving?

The root evil is financial opaqueness. Money management is reactive to most people. A bill comes in, you pay it. Your pay comes, the pay is spent. Nobody has actual figures but we make vague estimates such as, I guess I spend about 300 dollars on groceries. This results in financial stress and no savings objectives, as well as living on the edge.

This is solved using AI-powered tools that offer proactive, predictive and personalized financial oversight. They are a 24/7 pocket financial advisor, who will make sense out of the messy financial information into an action plan. They get you out of wondering What did you do with my money? to What can I do best with my money?

The All-in-One Financial Command Center: Copilot.

- Personal Story Hook: I would loathe the thought of putting my transactions into categories. Was that takeout Dining or Entertainment? Using Copilot, not only did I no longer worry, but the AI began to notice the patterns I had overlooked, such as my utility bills slowly going up, and I went on to find a better deal.

- What Problem It Addresses: Copilot addresses the issue of fractured financial consciousness.

- It integrates all your finances: checking, savings, credit card, investments, even loans, into a single, beautifully crafted, user-friendly interface. Its most remarkable aspect is a super-intelligent AI that studies how you spend money and classifies purchases in a frighteningly accurate way.

Step-by-Step Solution:

- Install and configure: Get the Copilot app (macOS and iOS with a version in development on Windows). The first arrangement is an interactive process.

- Link Your Accounts: Save your bank, credit card, investment, and loan accounts linked instantly and securely with Plaid, a reputable financial data aggregator. It is the read-only version so your money is secure.

- Get the AI to Learn: The first week, just inspect the automatic categorization offered by the AI. Fix any errors by hand; this trains the AI to your own preferences.

- Set Your Goals: Click into the “Goals” section. It could be a down payment, vacation or debt payment, set your goals and amount to save.

- Read Insights: Visit the Insights regularly. This is where Copilot AI comes in, providing such insights as “You are spending 15% more on dining this month” or, “You are on track to empty your Roth IRA.”

Common Mistakes to Avoid:

- Not paying attention to the Review: Do not simply set it aside and forget. Take 5 minutes weekly to look at the categories to ensure that the AI is learning correctly.

- Failing to use the Hold Feature: When you make a one-time purchase by large (such as a new laptop), you should apply the Hold feature to avoid throwing off your monthly spending reports.

- Connecting Compatibility Accounts: There may not be ideal connections between smaller credit unions or foreign banks. See the list of supported institutions to the extent that this is a concern.

My Personal Recommendation:

My best choice in this case is Copilot because this software is graphically oriented and the user can simply set it and forget about it as it becomes smarter with time. Its intelligent autonomy and design are the best. It functions as a subscription service (it costs about $13/month), but its insights will probably save you that much or even more.

Tally of the Debt Destruction Dynamo.

Personal Story Hook: I silently watched interest on my credit card silently killing my progress over the years. I was paying, but I was running on a treadmill. The Tally was the tool that eventually made me step off and automated a debt payoff strategy that I was too overwhelmed to handle myself.

What Issue Does It address: Tally addresses the expensive and intricate nature of credit card debt. It covers two primary concerns: 1) astronomical APRs that make it difficult to pay down the principal, and 2) the psychological strain of remembering several payment due dates, which also results in expensive late fees.

Step-by-Step Solution:

- Check Your Eligibility: Tally app can be downloaded and a soft credit check completed to determine if you qualify. To be approved as a Tally line of credit the minimum credit score required is about 580-600.

- Connect Your Cards: Securely connect the credit cards that you would like to pay off.

- Automate Payments: Tally will offer you a reduced interest line of credit when approved. It then takes these funds and automatically pays your higher rate credit cards on your behalf.

- Make One Simple Payment: You will now pay one monthly payment to Tally instead of having to pay several different card companies.

Common Mistakes to Avoid:

- Closing Paid-Off Cards: When Tally pays off a card, do not close the account at once. This could have adverse effects on your rate of credit usage. Simply chop up the card or lock it inside an application.

- Added New Debt: The greatest trap is to take the newly released credit in your cards to collect more debts. This nullifies this whole point. Physically locking away your cards may be an option to prevent temptation.

- Bypassing the small print: Learn how Tally charges. Although it is cheaper in terms of interest, you get charged a late fee in case you fail to make your payments to them.

My Personal Recommendation:

No one with good-enough credit and more than one high-interest credit card would not call Tally a no-brainer. It does the mathematically optimal “avalanche” technique of debt repayment without you needing to move a finger. It is a powerful financial robot and it has only one purpose: to make your debt vanish quicker.

The Hyper-Personalized Investment Coach: Magnifi.

Personal Story Hook: I wanted to begin investing more in favor of my personal values and interests, such as AI and robotics, but I simply did not have the time to research hundreds of ETFs and stocks. I have become a client of Magnifi, and have an AI investment assistant, who allows me to pose questions in plain English and receive a reply in the form of immediate and practical answers.

What Issue It Addresses: Magnifi helps to overcome paralysis in investment analysis. The universe of ETFs and stocks is enormous. As a retail investor, you might spend hours researching what funds best fits your strategy (e.g., “ESG tech companies with low expense ratios”). The AI of Magnifi does it in a few seconds.

Step-by-Step Solution:

Get the Magnifi App and View its Interface: Download and browse the interface without connecting to an account. Enter the conversational AI search engine.

Ask Your questions Investment: Type or Speak questions such as:

“Give me ETFs concentrating on artificial intelligence.

“Compare VOO and SPY.”

Find me a sustainable energy fund that pays dividends.

- Interpret Results: The AI will give you a list of recommended investments, fully furnished with primary data, performance graphs, and a simplified description of what the respective fund invests in.

- Trade (Optional): You have an option to open a brokerage account with Magnifi and directly use the AI to conduct research and place trades within the app.

Common Mistakes to Avoid:

- Mind the AI: The AI is not a financial advisor, it is a research tool. Always be your own due diligence when investing in real money.

- Overtrading: a tendency to do a lot of small trades on impulse can result because of the ease of doing so. Follow a basic plan and search with Magnifi the best instruments of that plan.

- Disregarding Fees: When using the inbuilt trading of Magnifi, you should know about the brokerage fees. See how they compare with your current broker.

My Personal Recommendation:

Magnifi suits the self-directed investor who believes in a long-term approach, but requires the initial research assistance. Imagine the Bloomberg terminal made user friendly by AI. It democratizes the provision of high-end investment research and makes it available to all.

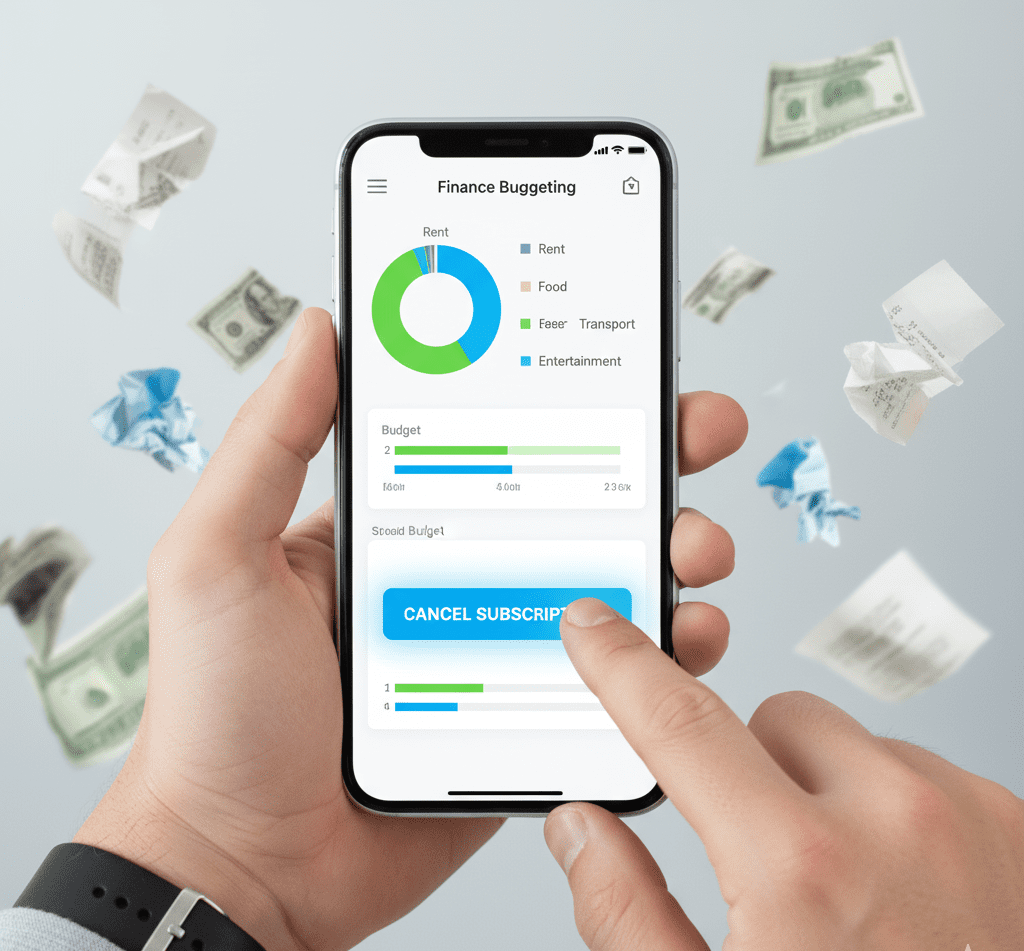

The Subscription Slayer: Rocket Money.

- Personal Story Hook: I was surprised when the AI of Rocket Money scanned my transactions. It discovered three subscriptions that I had totally forgotten about: a premium music subscription that I had not used in a year, an expired cloud storage subscription, and a monthly donation to a charity I liked but had intended to cancel. The savings were instant.

- Problem that it solves: Rocket Money is an assault on subscription bloat and wasteful recurring spending. These little monthly fees are the financial death by a thousand cuts, which quietly suck out of your bank account. It also offers strong budgeting, bill negotiation and net worth-tracking capabilities.

Step-by-Step Solution:

- Connect Your Accounts: Subscribe your bank and credit cards safe enough.

- Audit Your Subscriptions: The AI will automatically recognize and enumerate all of your subscriptions. As you can see they are all in one place with the monthly/annual cost.

- Cancel with a Click: Have a subscription you don’t use? Rocket Money will cancel it on your behalf with the press of a button, avoiding the burden of finding the cancellation pages.

- Apply the Budgeting Tools: Customize spending levels by allocating amounts to spending on items such as Food and Dining or Shopping. The application will provide you with automatic notifications when you are about to hit your limit.

- Try Bill Negotiation: Rocket Money experts will call your cable, internet or phone company to negotiate a lower bill on your behalf, a success-based service that costs you a fee of 30-40 percent of the savings.

Common Mistakes to Avoid:

- Everything at Once: Cancel. Unsubscribe to the services that you truly do not use, but do not deny yourself subscriptions that can add real value to you (e.g., your primary streaming service).

- Don’t forget to pay the Bill Negotiation Fee: The bill negotiation service is wonderful, but do not forget it is not free. Find out whether the net savings (less their fee) is worth it to you.

- Overlooking the Budget Alerts: Do not overlook the soft spending alerts. They are your red flag to avoid incurring extravagance before it strikes.

My Personal Recommendation:

Rocket Money (previously Truebill) will be a necessity of pretty much everyone by 2025. It has a powerful free version and is only worth the download thanks to its feature of subscription cancellation. It is the online version of a financial spring cleaning and its proactive notifications keep your spending habits on track.

My personal 2025 AI Stack in Personal Finance.

In my experience, I would construct an entire financial system as follows:

- The Brain (Awareness): Copilot is my main dashboard to all financial information and cash flow management.

- The Guardian (Spending): Rocket Money is my watchdog to subscription creep and budget bloat.

- The Destroyer (D): Tally is my auto-destruct at high interest debt (where necessary).

- The Grower (Investing): Magnifi is my research assistant in finding best ETFs and stocks to include in my portfolio.

This stack encompasses all areas of personal finance, including daily spending, long-term wealth generation, all automated by AI to save me time and maximize my money.

Q/A

Can I be sure that these apps will not access my bank account?

Indeed, with the right apps such as the ones below. They rely on trusted, read-only financial information aggregators such as Plaid. This is because they are in a position to view your transaction information but cannot transfer your money. They are encrypted with a 256-bit bank level encryption and do not store your banking logins.

I’m not tech-savvy. Am I going to be able to work with these AI tools?

Absolutely. The whole idea of these AI-based applications is to make money easier, not harder. They have intuitive interfaces, chatbots (such as the chat in Magnifi), and automating features that do the heavy lifting. There is a low learning curve.

Can the subscription fees justify these apps?

This is a crucial question. The response to this question is a resounding yes, provided they resolve a costly issue to you. Assuming that Rocket Money discovers and cancels 150 yearly unused subscriptions, its free version has already paid off. When Tally helps you to save 1000 dollars in interest on your credit card, its worth becomes evident. Perceive the charges as an investment, not a cost.

Will AI finance tools replace a human financial advisor?

These tools are certainly sufficient for most typical personal finance tasks, including budgeting, cost tracking, debt management, and simple investment analysis. However, only a human certified financial planner is invaluable when dealing with complex situations such as estate planning, strategic tax planning, and how to handle a financial windfall.